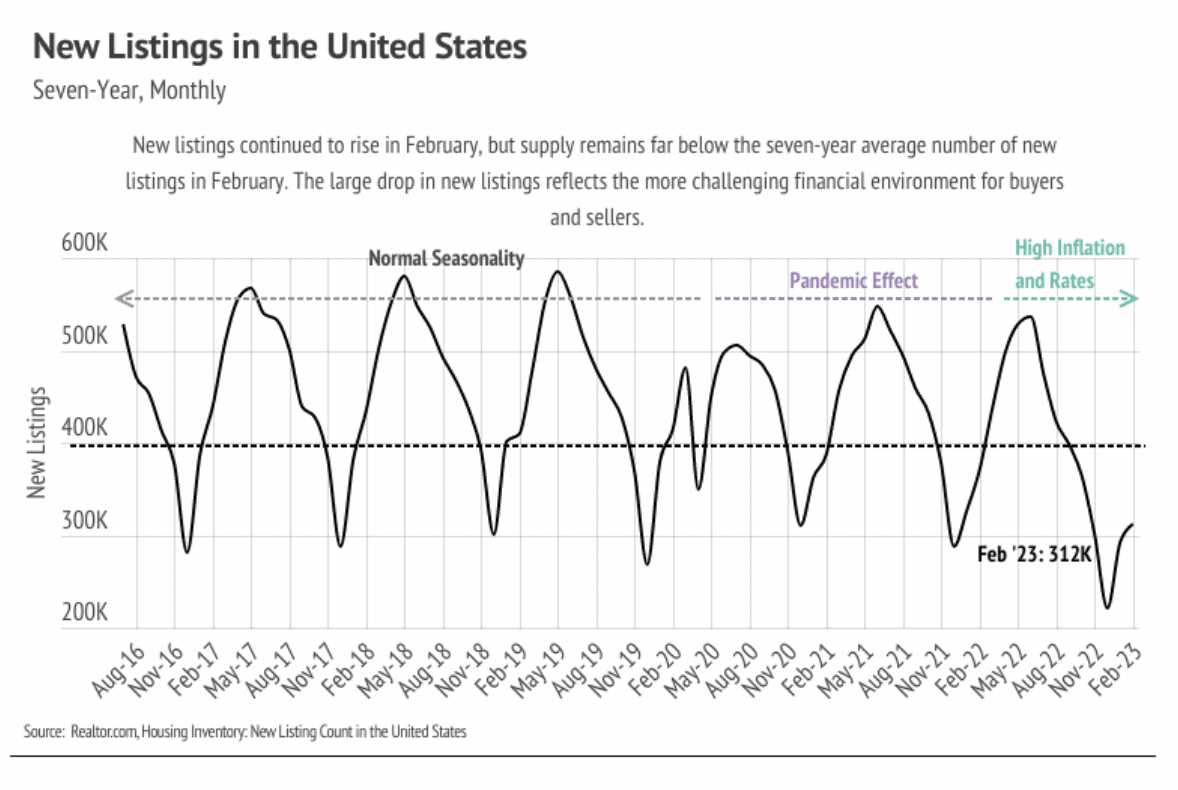

This time of year, we usually see both inventory and sales increasing steadily through mid-summer. Inventory is able to grow, even with increasing sales, due to the relatively high number of new listings that come to market in the first half of the year. However, the number of new listings actually decreased from January to February in all markets except for single-family homes in Orange County, which is an early sign that inventory will struggle to grow this year. Although we expect sales to be more muted this year, demand could start significantly outpacing supply, especially if sales continue to rise without being met by more new listings. Even with higher mortgage rates, the selected Florida markets are experiencing greater demand than much of the country for a couple of key reasons. People simply want to live in Florida, and homes are still somewhat affordable, which translates to more market participants.

Florida real estate has proven to be one of the most stable and resilient markets in the country. Single-family home prices have increased across the selected markets year over year, and looking back two years, prices have increased massively across counties. Miami-Dade condo prices fell year over year but have maintained much of the large gains in 2020 and 2021. Homebuyers in Florida can actually find a home within budget, which allows for a conventional loan to finance the purchase, and they can expect to refinance at some point in the future, which will decrease their monthly costs. The next three months will give us a clearer picture of how buyers and sellers are reacting to the current market conditions, but early signs point to more competition as we enter the spring season.

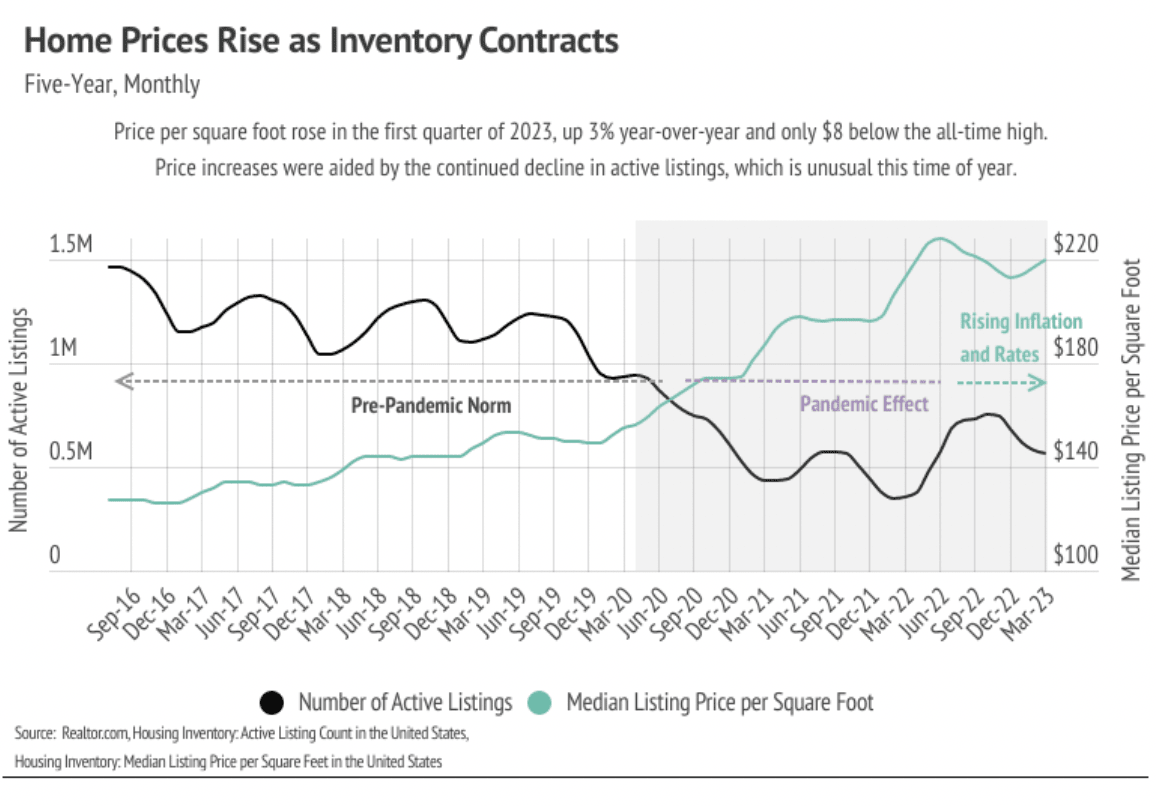

Inventory still historically low

Although single-family home inventory across markets is higher than last year, active listings fell precipitously in 2020 to what has become the new normal over the past two years. Inventory declined in February 2023 across markets and dwelling types with the exception of Broward County condos, which rose slightly. Higher interest rates have dropped incentives for potential sellers to enter the market, since sellers usually also must buy a new home. Homeowners either bought or refinanced recently, locking in a historically low rate, which means they aren’t selling and fewer listings are coming to market. Many potential buyers were priced out of the market as interest rates rose; however, interest rates have been higher for enough time that buyers are more comfortable re-entering desirable markets like Florida. Currently, buyers aren’t facing anything similar to the hypercompetitive 2020 and 2021 markets, but we will likely start to see more competition in the spring. New listings and sales both fell substantially year over year. We still expect some inventory growth in the first half of 2023, but inventory will likely remain low.

Months of Supply Inventory dropped, indicating a market shift

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes listed on the market to sell at the current rate of sales. The long-term average MSI is around four to five months in Florida, which indicates a balanced market. An MSI lower than four indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while an MSI higher than five indicates there are more sellers than buyers (meaning it’s a buyers’ market). MSI dropped in February, indicating that the markets are shifting toward more competitive for buyers. Currently, Miami-Dade favors buyers, Orange County favors sellers, and Broward County is more balanced. The sharp drop in MSI occurred due to homes selling more quickly and fewer new listings coming to market.

Local Lowdown Data